- Details

While consumer debt was rare just a few generations ago, credit card debt is now part of daily life for over 45% of Americans, according to the Federal Reserve’s 2022 Survey of Consumer Finances.1 Credit card debt is the most widely held type of debt in the US. But it doesn’t have to stay that way. Debt consolidation loans are a popular financial tool that can encourage borrowers to streamline their financial management and develop sound money habits.

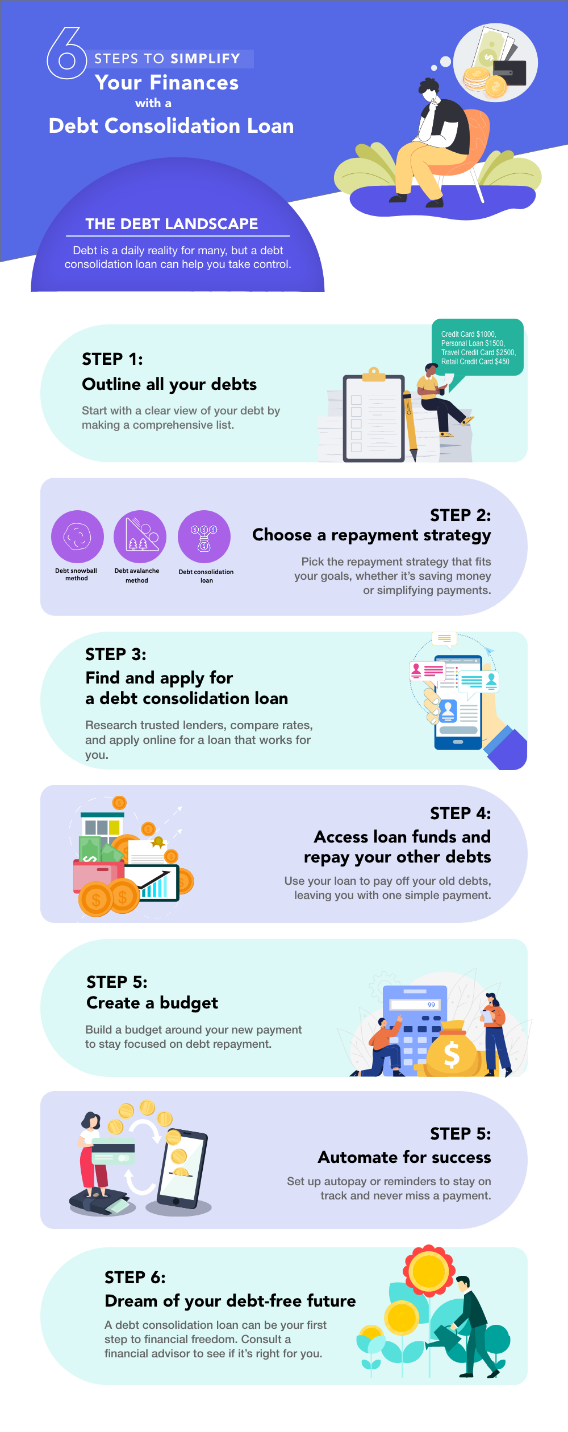

Here are six steps to simplify your finances using a debt consolidation loan.

- Outline all your debts

The first step in taking control of your finances is to take an honest look at your current debt burden. One of the best ways to do this is to create a list of your debts, being sure to include:

- Type of debt (credit card, auto loan, personal loan, mortgage)

- Current balance

- Interest rate

- Monthly payment amount

- Payment due date

- Lender

Certain types of debt, like a mortgage or auto loan, are likely not a primary concern when it comes to consolidating and paying off debt. Where you’ll want to focus is on high-interest consumer debt, like credit cards and personal loans, since these tend to have higher interest rates and can hold you back from pursuing other financial goals.

Once you list all your debts and have an honest look at how much you owe, you can begin to consider how you’ll repay them and which method makes the most sense.

- Choose a repayment strategy

There are several popular options when it comes to prioritizing debt for repayment.

Debt snowball

The debt snowball is a method of repaying debt that prioritizes paying your lowest balance debt first. As you begin the snowball, you’ll pay the minimum balance due on all debts, focusing your effort and extra funds on the debt with the smallest balance. Once that’s paid, you’ll move to the next largest debt, rolling any money you were previously putting toward the first debt into the second, and so on.

This cumulative effect creates a situation where you’re moving more quickly toward repayment with each debt that’s paid off. The idea behind the snowball is that a small win early in your debt repayment journey will motivate you to continue.

Debt avalanche

The debt avalanche is a debt repayment method that prioritizes paying your highest-interest debt first. With a debt avalanche plan, you’ll pay the minimum balance due on all debts, focusing your money and extra funds on the highest-interest debt, no matter the balance due. While the debt avalanche can save more money over time than the debt snowball, it can take years to see results from your efforts if your highest-interest debt is especially large.

Debt consolidation

The debt consolidation approach leverages a new, lower-interest loan to simplify repayment. With a debt consolidation loan, you’ll roll the balances of each debt into a single loan with a fixed interest rate. This means instead of prioritizing which debt to pay based on balance or interest rate, you’ll be able to devote all of your energy toward repaying a single loan.

Debt consolidation can be an effective strategy if the rate on the new loan is lower than the rates for the individual debts being consolidated. It’s also important to consider the term length of the new loan. Longer loan terms could actually increase the amount of money you’ll pay on interest over time, but can create a more manageable monthly payment today.

- Find the right debt consolidation loan and apply

If debt consolidation is the right choice for your financial situation, it’s time to research lenders and apply for a loan. You’ll want to look for a reputable lender with great customer reviews and a history of successful borrowers. Thanks to the rise in online lending, applying for a personal loan is a simple process that can be done 100% online with many lenders.

- Receive funding and repay other debts

If you’re approved for a debt consolidation loan, your lender may send funds to your existing creditors directly to repay what you owe or give you the money to do so. Once you repay those other debts, you’ll be responsible for the monthly payment for your new debt consolidation loan.

- Create a budget that includes your debt payment

To effectively manage your debt consolidation loan over time, you’ll want to ensure you incorporate your new, fixed loan payment into your budget. Having a single number to hit every month can increase your focus on the goal at hand and hopefully motivate you to get serious about getting out of debt for good.

- Set yourself up for success

Once you create your budget and ensure the money will be in your account on time each month, you’ll want to set yourself up for continued success by setting payment reminders or setting up automatic payments. Autopay can take the guesswork out of managing your loan, leaving you with more time to focus on earning more and developing good financial habits.

The bottom line

No matter the reason you ended up in debt, there’s no time like the present to change the financial future for you and your family. A debt consolidation loan can help you streamline financial management and shift overwhelming debt into a single monthly payment. If you’re not sure about whether a debt consolidation loan can help you, consult a financial professional to discuss the pros and cons with your unique financial needs in mind.